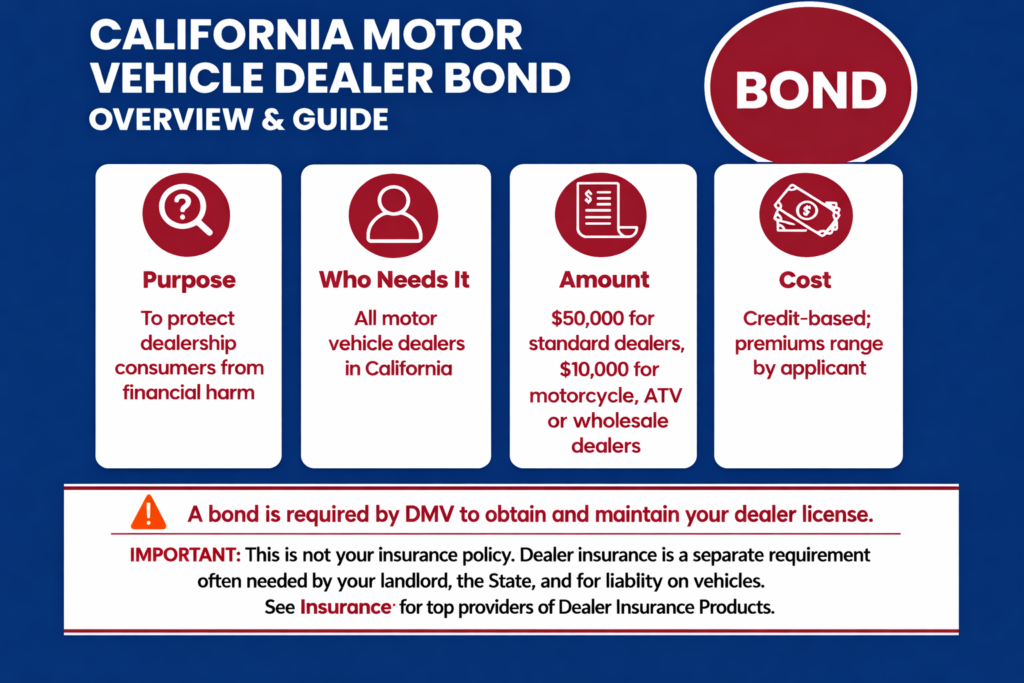

Motor vehicle dealers are required to carry and maintain a Surety Bond, commonly referred to as a Dealer Bond.

Get Your Bond NOW!

Motor vehicle dealers are required to carry and maintain a Surety Bond, commonly referred to as a Dealer Bond. This bond is issued by a surety company—usually an insurance carrier or financial institution—that guarantees the dealer’s obligations.

If a dealer commits fraud or violates the law, an affected party (a consumer or the state) may file a claim against the bond. When the claim is legitimate, the surety pays out up to the bond amount. The dealer must then reimburse the surety for whatever was paid.

Get your Bond Quote NOW:

Enter Business name, State, type “Dealer”: Find the $10,000 (Wholesale under 25 vehicles per year) or$50,000 Retail Bond < Most Common

City of Hawthorne requires an additional bond**

It may take up to 1 or 2 business days to obtain your bond –

Dealer bonds play a critical role in maintaining confidence in the industry. They assure regulators and customers that a dealer will conduct business ethically and legally, and they provide a financial remedy if the dealer fails to do so.

Bond Vs. Insurance

A surety bond is not an insurance policy. It guarantees compliance with statutory obligations but does not provide coverage for the dealer’s liability, property damage, or business operations.

Key Differences

To understand why they are treated distinctly, consider their core purposes:

Surety Bond: Protects the public and the state. If you fail to deliver a clear title or commit fraud, a claimant can collect from the bond. However, the bond company will legally require you (the dealer) to repay every dollar they pay out on your behalf.

Liability Insurance: Protects your business. It covers claims like customer injuries on your lot or property damage from test drives, and it does not require you to reimburse the insurance company.

Who Requires Dealer Liability Insurance?

Because a surety bond only covers specific regulatory and financial compliance, other entities typically require you to carry separate commercial liability insurance:

State Licensing Authorities (DMV / Dealer Boards): Many states explicitly require auto dealers to hold garage liability or general liability insurance in addition to the state-mandated surety bond to protect against physical damages and accidents.

Floor Plan Lenders: If you finance your inventory, lenders will mandate garage liability and dealers open lot (DOL) insurance to protect their collateral.

Landlords: If you lease your dealership property, your commercial lease agreement will require general liability insurance.